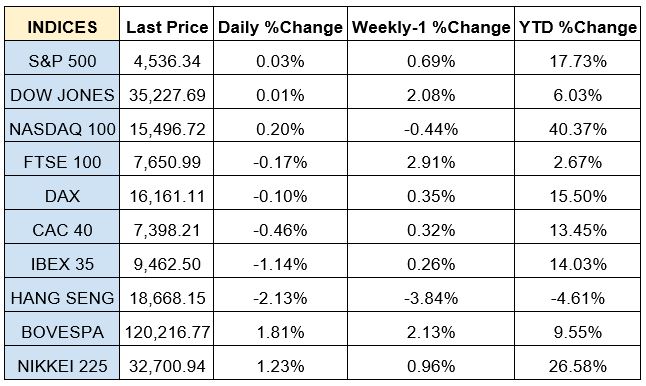

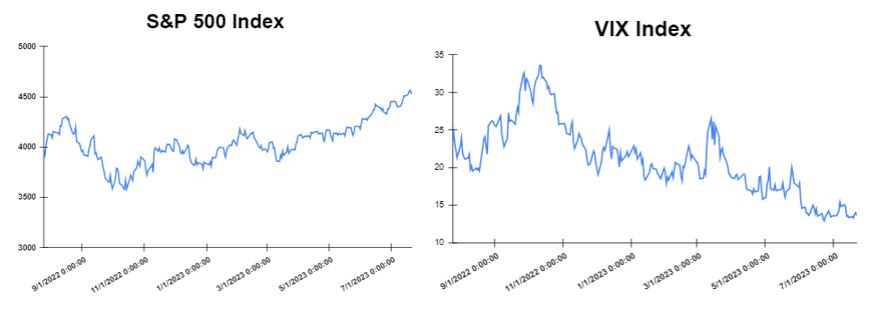

Global markets finished the week almost higher

The global markets started the week mixed, , following the massive gains of last week and investors waiting for the incoming economic data. There were not any important data releases on Monday, except for the monthly report of the Deutsche Bundesbank, which showed that the German economy is likely to have recovered slightly in the second quarter of 2023. On Tuesday, the strong earnings gains of the companies turned into gains for the US market. Also, the U.S. retail sales contributed to these gains as they rose less than the forecast for the month of June. On Wednesday, Global markets closed mixed as the annual inflation in the United Kingdom rose by 7.9% on a yearly basis in June. On the same day, the annual inflation rate in the Eurozone (EA20) stood at 5.5% in June, down by 0.6 percentage points compared to the previous month. Also, the U.S. housing data, which are still under the weight of rising interest rates, came in below expectations. On Thursday, the Nasdaq decreased sharply as Tesla and Netflix reported weaker-than-expected Q2 earnings results. Also, the Initial jobless claims in the United States for the week ending July 15 went down by 9,000 compared to the previous week’s revised figure to come in at 228,000. Furthermore, Producer prices in Germany increased by 0.1% year-on-year in June, with the index being 0.3% down in comparison to the previous month. On Friday there were no U.S. economic releases. In Europe, retail sales volumes in the United Kingdom in June rose by 0.7% compared to the month prior. Finally, the Global markets closed almost higher as investors followed a week of data and corporate earnings. The Dow Jones closed flat at the closing bell on Friday. The S&P closed flat. Furthermore, the DAX declined by 0.17% and the CAC 40 jumped by 0.63%. The FTSE 100 gained 0.20%.

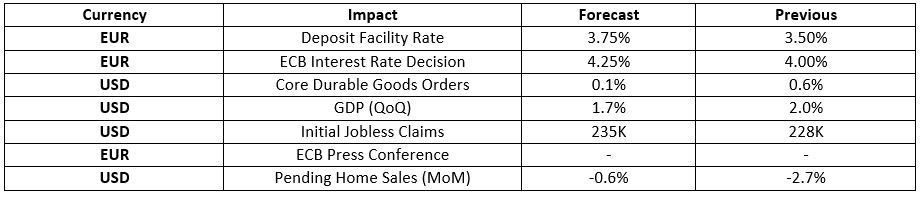

In addition, investors are looking forward to the ECB Interest Rate Decision which is expected to increase to 4.25% from 4.00%

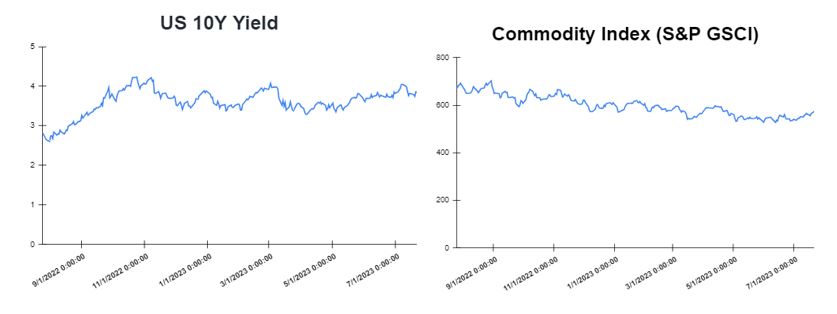

Treasury yields were almost flat towards the end of the week

Yields were higher at the start of the week as investors awaited the economy and monetary policy ahead of a week with few key economic data reports. However, yields moved lower on Wednesday as investors assessed the global economic outlook especially regarding inflation and how it may affect monetary policy after several countries posted their latest inflation figures. On Friday, yields closed the week flat as investors weighed what could be on the horizon for interest rates ahead of the Federal Reserve’s meeting next week. Specifically, on Friday, the yield on the 2-year Treasury decreased to 4.844%. Short-term rates are more sensitive to Fed rate hikes. The 10-year Treasury yield, hit 3.837%, down by about 2 basis points. The 30-year Treasury yield, which is key for mortgage rates, hit 3.9070%. The spread between the US 2’s and 10’s advanced to -100.7bps, while the spread between the US 10-Yr Treasury and the German 10-Yr bond (“Bund”) advanced to – 148.0 bps

In addition, investors are looking forward to the Fed Interest Rate Decision which is expected to increase to 5.50% from 5.25%

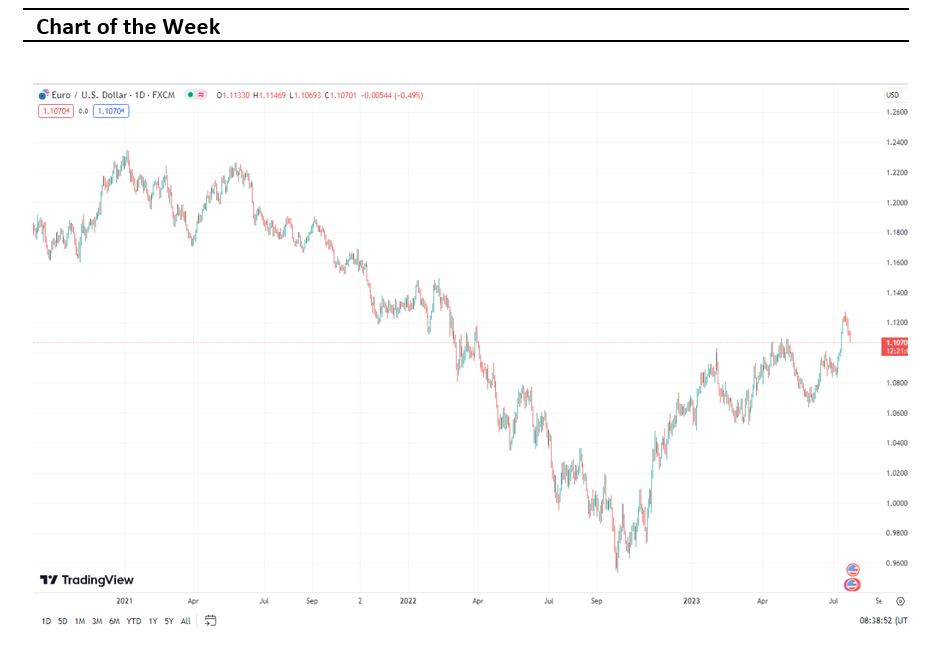

Volatile week for USD

The US Dollar at the start of the week was lower affected by the stronger-than-expected July Empire manufacturing. In the middle of the week the US Dollar advanced as UK Core CPI eased for the first time since January from 7.1% YoY to 6.9% YoY and service inflation fell from 7.4% YoY to 7.2% YoY. However, on Friday, the US dollar finished higher after the sharp decline of the previous week, supported by US economic data. The EURUSD decreased to 1.11, while the GBPUSD decreased to 1.2850. Additionally, the USDJPY increased to 140 Yen on Friday.

Oil and Gold traded mixed towards the end of the week

Gold started the week lower amid a solid recovery in the US Dollar Index (DXY). However, Gold traded lower at the end of the week as investors focus their attention on the Federal Reserve (Fed), which is likely to resume its policy tightening spell next week after skipping in June. On the other hand, oil prices decreased on Monday as supply pressures seemingly eased following media reports that oil production in Libya will partially resume following the protests last week that forced the closure of three key oilfields. However, oil finished higher at the end of the week, as supply woes seemingly continued to dominate the crude market sentiment. Meanwhile, this week’s report by the United States Energy Information Administration showed that the crude oil inventories in the country declined by 700,000 barrels. Meanwhile, the Crude Oil Inventories report will be released on Wednesday which is expected to show a decrease of 1.692M.

Stock indices performance

Key weekly events:

Monday -24 July 2023

Tuesday – 25 July 2023

Wednesday – 26 July 2023

Thursday – 27 July 2023

Friday – 28 July 2023

Sources:

https://www.tradingview.com/

https://breakingthenews.net/Home

https://www.investing.com/

https://www.fxstreet.com/news

https://www.cnbc.com/world/